Over the past six years, I’ve gone from having one credit card to having more than half a dozen. With every card I add, I often pick up an extra perk, multiplier on a useful category, or some other benefit. Meanwhile, as my portfolio evolves and as issuers update their products, there are also some instances where a card no longer becomes useful to me.

With all of that in mind and as we look to the new year, it’s time for a look at the cards I’ll be carrying in 2023 and how I’ll be making the most of each of them.

What Credit Cards I’m Using in 2023 and Why

Bilt Mastercard

What I’ll Be Using it For in 2023: Rent, “Rent Day” purchases, and at least 5 transactions a month

The newest addition to my credit card line-up is the Bilt Mastercard. Incidentally, the card also has the most easily defined purpose in my mix: rent. Yes, this unique offering not only offers 1x on rent payments but also uses a clever technique to help customers avoid paying the fees typically associated with paying rent on a credit card.

Alas, there is a small catch when it comes to Bilt. In order to earn any points for the month, you’ll need to make at least five purchases on the card for that statement cycle. Presumably, this is so that people don’t just use it for rent and keep it in their sock drawer otherwise. Luckily, I haven’t found this requirement to be too taxing — especially since the 3x on dining is competitive enough that I’m not really missing out on much to use it a few times for these purchases.

Also helping me get to that five transition requirement is the Rent Day promotion Bilt introduced a few months back. Now, on the first of each month, cardholders can earn double points on everything… except rent. So, suddenly, I can earn 6x on dining for the day while also earning 2x on pretty much whatever else I buy. With all of these factors at play, the Bilt Mastercard could well be the most consequential addition to my wallet in years.

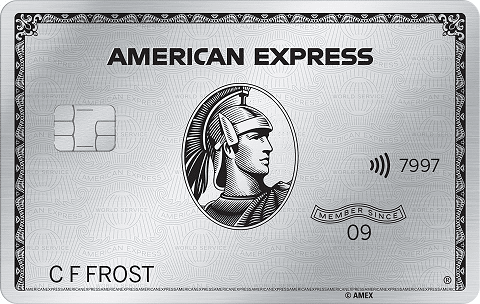

American Express Platinum Card

What I’ll Be Using it For in 2023: Amex Offers, special credits, travel bookings, and travel perks.

Speaking of consequential, I recently wrote about why I felt the Amex Platinum was still worth it to me even after being hit with the $695 annual fee for the first time (previously, it was $550). In that write-up, I detailed how the numerous credits the card offers coupled with key perks, such as airport lounge access still meant that I was getting value from the card despite the fee. Unsurprisingly, my feelings haven’t changed much in the past few months, meaning that the Platinum card will retain its place in my wallet for 2023.

With that said, it does seem likely that I’ll be using the Amex Plat less for actual purchases and more for credit redemption and the occasional Amex Offer. That’s because, while the card offers 5x on flights booked directly with the carrier or via Amex Travel as well as 5x on hotels booked via Amex Travel, there are other travel redemption opportunities I’ll have available to me thanks to some of our other cards. So, the question may often be, “Do I want to earn 5x or redeem points elsewhere?” In any case, I’m sure the Platinum card will still see plenty of use in the new year and beyond.

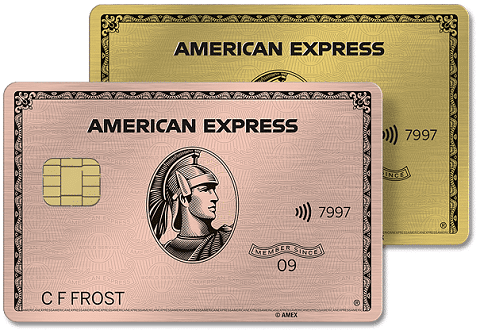

American Express Gold Card

What I’ll Be Using it For in 2023: Most dining and grocery store spending, as well as using associated credits.

If the Platinum card is the perks card then the Gold card is the workhorse in my Amex duo. With 4x on dining and 4x at U.S. supermarkets, the card wins both categories in my portfolio. Obviously, that makes it one of my most-used cards, which is also why it literally has a primo spot in my wallet.

Of course, that extra 1 point per dollar spent doesn’t exactly justify the $250 annual fee on its own (at least not for me). That’s where the Gold card’s credits come in. First, there’s the $10 a month in Uber Cash that pools nicely with what I get from the Platinum card. Typically, my wife and I will use these funds to place an Uber Eats pick-up order during the month or, if we’re traveling, we’ll use it for actual Uber rides. The other credit is a $10 Dining Credit, which is a bit harder to use. If we had a Shake Shack near us, it’d be no problem. Unfortunately, we don’t — so this credit is usually used for a Grubhub pick-up order or, on occasion, a Goldbelly order.

Seeing as those two credits make for an effective annual fee of just $10, it’s definitely worth keeping the Gold card around. However, if something were to change with those credits — especially the Dining Credit — that would make them harder for us to use, I could see having to part ways with the card down the road. Until then, though, we’re racking up Membership Rewards points with this one.

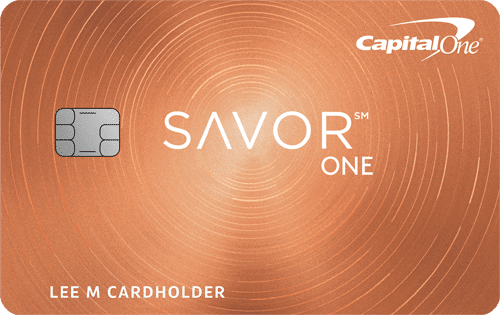

Capital One SavorOne

What I’ll Be Using it For in 2023: Entertainment, occasional restaurant spending, and foreign spending

To be honest, the Capital One SavorOne is a card that has lost a lot of its usefulness in my wallet over the past few years. Don’t get me wrong — I think it’s one of the best no-annual-fee cards on the market. However, with so much overlap with the Gold card, it doesn’t always rise to the top in my mix. Nevertheless, the card does have some superpowers to speak of.

First, while the Gold card’s 4x category applies to dining, the SavorOne’s 3x applies to dining and entertainment. That latter category is crucial for us as Disney Parks and theme park fans as we’ve been able to earn 3% back on annual pass purchases, runDisney race registrations, and more. Plus, the SavorOne also earns 3x on select streaming service purchases, which is why we recently charged our Disney+ subscription to it.

On top of that, the SavorOne continues to be a great option for when we’re traveling internationally. Since Amex isn’t quite as widely accepted as Mastercard overseas, our SavorOne card is one of our go-tos while abroad. And, since the card has no annual fee and is a cashback option, I have no problem keeping it in our mix even if we may not be using it to its full potential.

Chase Sapphire Preferred

What I’ll Be Using it For in 2023: Generic travel purchases and some regular spending

I’ll fully admit that, when we picked up the Chase Sapphire Preferred, it was purely because of the 100k intro bonus that was being offered at the time. Yet, when renewal time came around, we decided to stick with it. Why? Partly due to laziness — and partly because the card’s revamped benefits, such as a $50 Annual Ultimate Rewards Hotel Credit, seemed to make sense.

Despite this, when I went to type what I’d be using this card for in the new year, I kind of drew a blank. Yes, the card’s 2x on generic travel purchases category is somewhat helpful and is a bit broader than Bilt’s travel category, but that’s really about it. Well, that is until you consider that the Preferred’s points can be redeemed via the Chase Ultimate Rewards travel portal at a rate of 1.25¢ each. That means that even 1x spending could effectively be 1.25x if we wanted (note: same with Bilt). With an annual fee of $95, we really do need to figure out a better plan for this card in the long term — although the aforementioned $50 credit does take the effective annual fee down a bit. For now, though, we’re still giddy about all the points we earned when we first opened the card.

Apple Card

What I’ll Be Using it For in 2023: Non-category Apple Pay purchases, T-Mobile bills, foreign transactions

Lastly, I’m once again going to defend the Apple Card. Seeing as I don’t have a flat 2% cashback card in my mix, this one often steps into that role whenever Apple Pay is available. Plus, thanks to the 3% back on T-Mobile purchases category, I’m saving a decent amount on my phone bill each month with the card.

The other big perk I’ve found with this card is overseas. As I’ve written about before, in my experience, using Apple Pay internationally is often much easier than using physical cards in terms of speed of transaction and the likelihood of getting declined. So, if I can earn 2% back while encountering no foreign transaction fees, it seems like a win to me.

If I may look further into the future, however, one threat to my Apple Card would be if I even ended up pulling the trigger on the U.S. Bank Altitude Reserve card that I’ve been eyeing for literally months now. With that card, all of my mobile wallet purchases would earn 3x compared to Apple’s 2%. But, until that happens, the Apple Card remains in my digital wallet.

For the complete list of the highest rated credit cards with all of the latest offers click below.

Overall Thoughts on My 2023 Credit Card Strategy

Dining dilemma

All things considered, dining is a solid category for any credit card to offer multipliers on. As a result, it seems that a lot of them do just that. For me, this means that I now have at least three cards competing for my restaurant spending. At the top of the list, there’s the Gold card’s 4x, while the SavorOne, Bilt Mastercard, and Sapphire Preferred each have 3x. Given the Bilt card’s requirement that I make at least five transactions per month, it probably gets the edge in my backup pick. Then again, the Sapphire Preferred’s points can be redeemed at a 25% bonus for travel and the SavorOne is my only true cashback option in this situation, which still keeps both of them in the mix. Ultimately, it will likely continue to be a game-time decision for me, but one thing is clear: I don’t really need any more dining cards!

Another new currency

Although I may not have fully realized it at the time that I applied, adding the Bilt Mastercard to my wallet now means I’m operating in three different point currencies in addition to cashback setups. Foolishly, I kind of assumed that Bilt would have a simple 1¢ per point cashout option a la Chase or cashback cards. Instead, there’s actually not even a true cashback option and the redemption rates for other activities vary widely. For example, while you can redeem points toward future rent payments, this only assesses the points at a measly 0.55¢ each. Meanwhile, the best option is technically the “down payment on a house” one, which values points at 1.5¢ each. Short of that, the second best option on paper is the Bilt Travel portal, which offers 1.25¢ per point.

Of course, like other point currencies, Bilt also offers a stable of transfer partners. What’s more, there is some overlap between their transfer options and those of other cards. From what I can tell, there are currently seven programs that are transfer partners with all three of my currencies, Amex, Chase, and Bilt. Additionally, there are another three common partners between Amex and Chase, three more between Chase and Bilt, and two others between Amex and Bilt. So, although having three different currencies may not be ideal for someone like me, it is still fairly manageable for now.

Managing payments

Okay, so the rewards that come with using multiple credit cards can be great. On the other hand, the reality of keeping up with billing cycles and payment due dates can be a pain at times. Luckily for us, we’ve been pretty good about opting into all of the available reminders — or, even better, paying off a balance as soon as the statement closes to prevent issues. Still, my biggest concern about adding even more cards would be in terms of keeping on top of the payments and not screwing myself over.

Even though my credit card mix didn’t change tremendously from last year (with only one card added), I am still learning more about how to best use each of the cards I have. Furthermore, while I wouldn’t say I really need another rewards card, I do have a few ideas in mind that might be able to slot into my mix. Will those options or others make their way into my 2024 card portfolio? You’ll have to stay tuned!