It was a mere few weeks ago that I woke up to discover that the investment app Robinhood was introducing a Checking & Savings product that promised to pay account holders 3% interest. Being an active Robinhood user (and having reviewed the app previously), I jumped at the chance to sign up and even managed to snag a spot in top 100,000. Moreover, the more I looked into proposed offerings, the more excited I became. Access to 75,000 free ATMs along with the absence of a monthly, minimum balance, even foreign transaction fees were all part of the package, topped with a snazzy-looking debit card for a bow. Unfortunately, things took a major turn soon after this announcement and haven’t rebounded since.

So what’s going on with Robinhood’s Checking & Savings plan and what does it mean for the app itself? This is something I’ve been thinking a lot about lately and I feel like I should address. From a recap of the controversy to reconsidering the app and offering alternatives, let’s dive into what I’m calling “The Robinhood Debacle.”

Robinhood’s “Checking & Savings” Controversy

Robinhood’s “Checking & Savings” Controversy

What happened with Robinhood’s announcement?

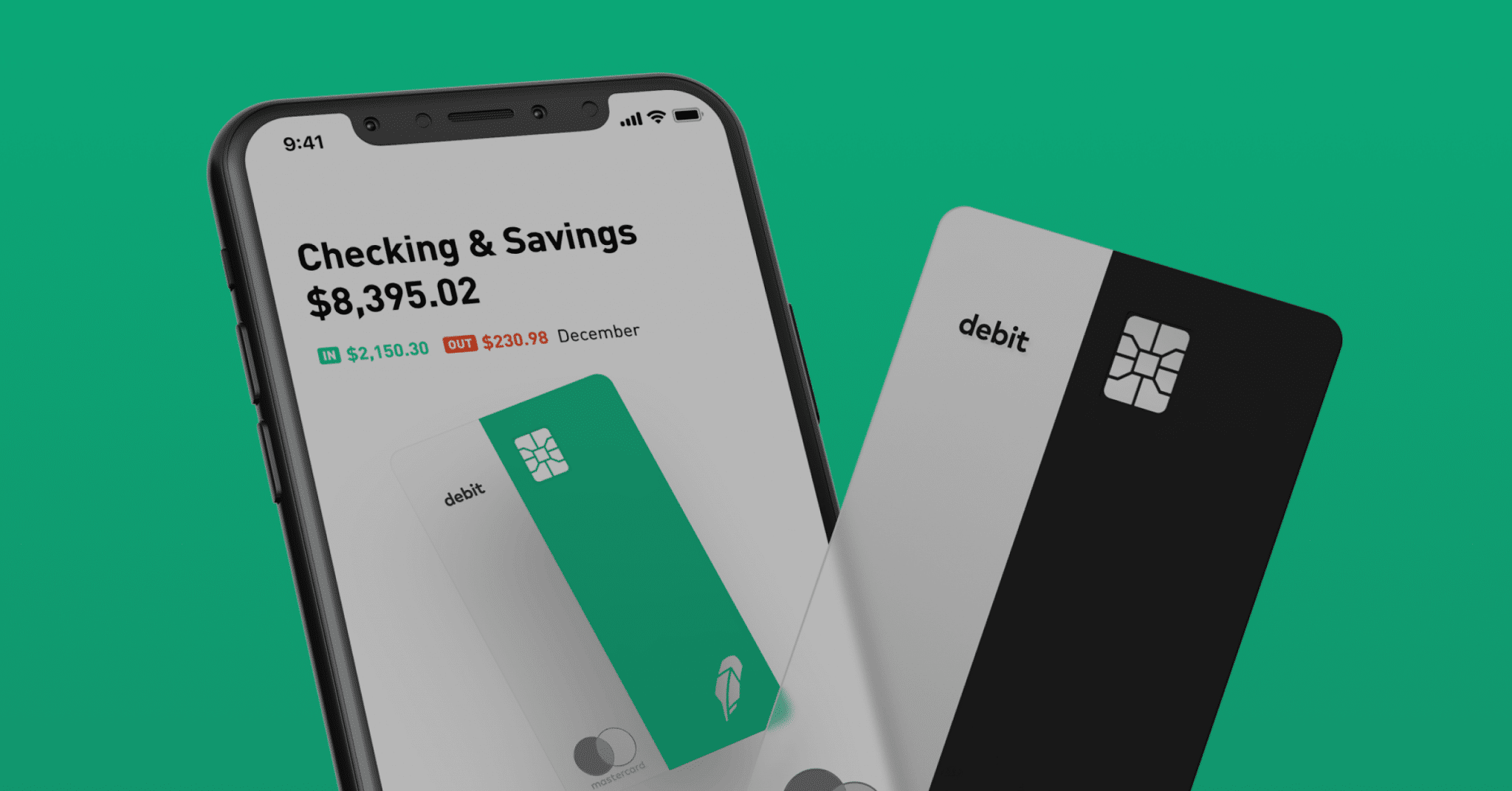

First things first — Robinhood announced its so-called Checking & Savings product on December 13th, 2018. As mentioned, most headlines included the fact that the offering would pay out 3% interest on funds but also noted that they’d steer clear of fees that most other banks charge such as overdraft fees and minimum balance fees. On top of that, materials for the new product indicated that users wouldn’t be required to trade stocks in order to maintain a Checking & Savings account with the company. Needless to say, all this led to a flood of current and new users joining the waiting list (making my seeding at around 68,000 all the more impressive).

Not 24 hours after this announcement was made, some bad news arrived in the form of Securities Investor Protection Corporation (SIPC) head Stephen Harbeck telling the media that not only did Robinhood execs not inform him of plans for the new product, but also that he had some serious concerns about the offering. Lest you think Harbeck was just upset that he wasn’t kept in the loop, he went on to note that, based on the materials Robinhood had released, it seemed as though these types of accounts wouldn’t be covered by SIPC insurance despite the app asserting that they would.

Long story short, later that evening, Robinhood co-CEOs and co-founders Baiju Bhatt and Vlad Tenev released a letter somewhat apologizing for the confusion their announcement caused. In it they said, “As a licensed broker-dealer, we’re highly regulated and take clear communication very seriously. We plan to work closely with regulators as we prepare to launch our cash management program, and we’re revamping our marketing materials, including the name.” Around the same time the app and website were updated to read “Cash Management – Coming Soon” instead of “Checking & Savings – Coming Soon.” The app continued to allow waitlist sign-ups for the product via a newly-added tab but that tab was quietly removed sometime over the weekend of December 29th. At last check before its removal, the waiting list had grown to nearly one million. Still, Cash Management is still referenced both in the account section of the app as well as on the company’s main site.

What happens now?

That’s a great question. When the switch from “Checking & Savings” to “Cash Management” occurred, images of the Mastercard debit cards that were part of the product disappeared as well. Before the SIPC’s comments, Robinhood has stated that the first cards would be shipping in January 2019 (AKA this month). That timeline hasn’t been referenced since. However, when users questioned the company’s official Twitter account about the tab’s removal, they referred them to the founder’s letter and continued to say that the revamped product would arrive this year.

To be clear, launching a product like this without SIPC support or insurance hardly seems like an option for the app. Instead a more likely scenario would find the app introducing many of their same plans but finding a model that adheres to what SIPC insurance is intended for, meaning that some sort of investment and purchase of securities would be required. Interestingly, while appearing on CNBC, Robinhood CEO Bhatt said that part of the company’s plan with this product was to invest customer cash in “government-grade assets” that he believed would return profit in excess of the 3% that would be paid to customers. If that’s the case it seems a modified and more transparent version of that idea might qualify for SIPC coverage — but this is pure, unfiltered speculation on my part.

The Fallout from Robinhood’s Misstep

The Fallout from Robinhood’s Misstep

Can Robinhood be trusted?

When I first saw stories about SIPC taking aim at Robinhood’s announcement, I first thought it was just a case of disruptors disrupting — something I’m mostly a fan of, for the record. That said, once I actually looked at the issue at hand, my opinion shifted strongly. In fact, it’s safe to say that it may have changed my perspective on Robinhood itself.

I came to realize that, while there are several finance-related apps I use to track my spending, earn cash back, or even store money, Robinhood is a bit different from all of those because it involves trading stocks. Even though I keep savings apps like Clarity Money and Long Game, I know those funds can easily be withdrawn without penalty or loss (not to mention that they’re also FDIC insured). But with Robinhood, if they were to announce that they were dissolving, I’d likely be forced to sell my current positions — potentially at a loss. To put it bluntly, it makes you wonder if the free trades that Robinhood provides are worth that risk.

Let me back up a bit and assure you that Robinhood’s brokerage accounts are SIPC insured. Thus there’s little reason to think you’d be completely hosed if the app were to go under. Still it’s not a great feeling when the company run afoul of the very organization their users depend on for such peace of mind.

What alternatives are there?

Something Robinhood deserves a lot of credit for is that they’ve shown that stock trading isn’t just for the wealthy — or at least it shouldn’t be. In recent years, many alternative brokers have popped up with greatly reduced trading fees. Among them, Fidelity Investments offers stocks and ETFs at a fee of $4.95 per trade. Meanwhile Chase recently rolled out commission-free trades to account holders, allowing them to trade up to 100 stocks or ETFs in their first year fee-free. As a result it’s not hard to imagine that some of those who dipped their toes into investing thanks to Robinhood might now look to these other platforms following this controversy.

As for a Checking & Savings/Cash Management alternative, there are several online banks that offer at least part what Robinhood was promising. I actually have both a checking and savings account with Discover Bank that includes some free ATM access, 1% cash back on debit transactions, certain waived fees, and (currently) 2% APY on savings. That might not be quite as good as 3% like Robinhood was advertising but it certainly beats most brick-and-mortar banks. Another online bank I’ve looked at but haven’t personally joined is called Aspiration. Looking at their site, it says they allow you to use any ATM — either in the U.S. or international — without a fee. Plus they offer 1% interest on your money. Like I said, I haven’t tried this one out for myself but it seems like another potential option.

The Bottom Line

Personally, at this time, I do still find myself believing in and trusting Robinhood’s core product and will continue to trade stocks with the app. Furthermore I truly hope that the company and the SIPC are able to work things out and launch a version of Cash Management that includes what Robinhood promised, while also passing the SIPC’s requirements for insurance. At the same time, this whole ordeal has opened my eyes to some of the risks associated with utilizing financial startups — something I had grown all but immune to having spent so much time using them.

To me, it boils down to this: if you no longer feel comfortable using Robinhood, then don’t. If you do feel comfortable, it’s probably still a good idea to retain some skepticism and ensure you’re not endangering your livelihood by putting all your eggs in one basket. In either case there are alternatives you can use to invest your money, getting a better return rate on your extra cash, and more.