First the bad news: considering all the major data breaches that have hit retailers, websites, and freaking credit bureaus alike, there’s a very strong chance your personal info has been compromised at some point. Luckily, in addition to steps you can take, such as freezing your credit reports to prevent criminals from using this data, there are a growing number of tools you can use to foil thieves in the future. Add to this list Privacy.com, which allows users to create unique card numbers they can use to conceal their actual info.

Beyond the ability to keep your credit card info safe, this free service also has the potential to save you money. Let’s take a closer look at how Privacy.com works and how this tool could benefit your financial life.

- Cards can be created for one-time use

- Spending limits and other features are perfect for free trials and more

- Funding source must be a debit card or bank account

- Some users report negative experiences

Getting Started with Privacy.com

Signing up

Just like with most websites you encounter, joining Privacy.com starts with you entering your email address and creating a password. Naturally, you’ll also be asked to verify that email address to prove you do, indeed, have control of it. This part of the process is so commonplace that I doubt most would think twice about it. However, it’s the next step that may give some individuals a moment of pause.

In order to create card numbers using Privacy.com, you’ll need to link a funding source that will be tapped whenever one of your proxy cards is used. To link a funding source, you’ll need to select your bank and log into your online banking account. Even for a site with “Privacy” in its domain name (or perhaps especially because of this), first-time users might be a bit hesitant about this aspect of the sign-up process. That said, those who have ever linked their bank accounts on other personal finance apps and sites will surely recognize the banking APIs employed here. This helped ease my worries but I still understand those who might not want to give this info up.

Once a funding source is linked, you’ll be able to start creating cards. You can also link additional funding sources and select which account you’d like each card to pull from. Something to note is that, at this time, funding sources can only be bank accounts and debit cards. Credit cards are not currently supported.

Creating new cards

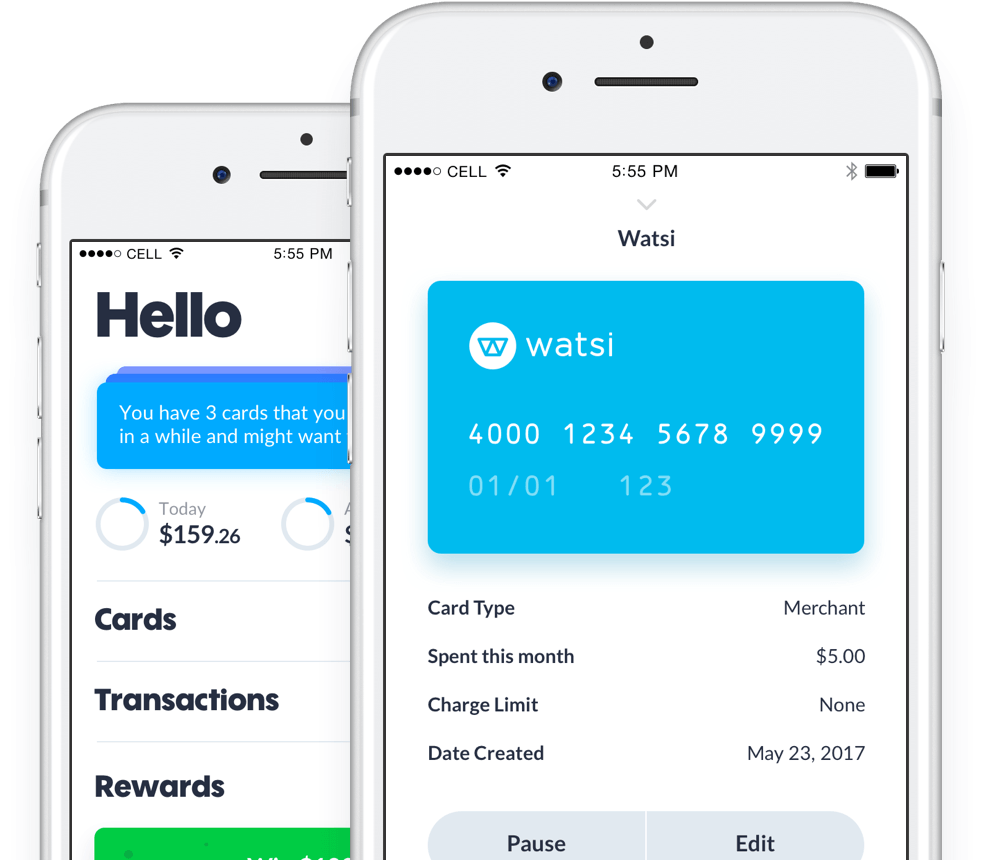

When you log into Privacy.com, on the left side of the screen, you’ll see a section that’s now simply labeled “Cards.” This is where you’ll not only see any cards you’ve previously created but it also has a link to make new ones. These cards can either be assigned to a certain recurring expense (e.g. Netflix, iTunes, Spotify, etc.) or you can create single-use “burner” cards.

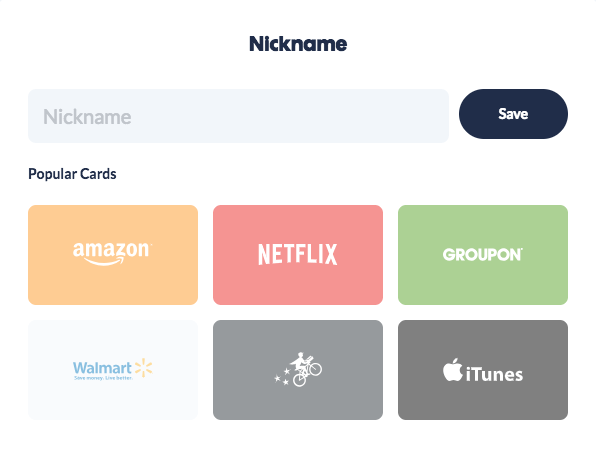

To set up a new card, you’ll first want to assign a nickname to your card to help remind you what it’s used for. As part of this process, you can also select from a library of commonly-used logos in order to make it even easier to identify which card is which.

For example, Amazon, Postmates, and Groupon are among some of the popular card design options you’ll see when assigning a nickname. To further customize your digital cards, you can decorate them with emojis or icons to help you remember what each is for.

After naming your card, you can select a spending limit. These limits can be per transaction, per month, per year, or total. So, if your Netflix bill is $10.99 a month, you can set your card to decline any transactions over $11 (note: it seems Privacy.com only allows limits to use whole numbers and not decimals). You can also create a “burner” card by selecting the “single-use” option at the bottom of the Spend Limit window. Regardless of whether you’re setting up a recurring limit or a single-use card, just hit “Save Limit” when you’re done to move onto the last step.

As I mentioned, you can link multiple funding sources for use on Privacy.com. Thus the final step in creating a new card is to confirm which source you want the card to utilize. After that, you can hit “Create Card” and you’ll see it join your wallet.

FYI, with the basic (free) plan, you can create up to a dozen cards a month.

Using your Privacy.com cards

There are a few different ways you can utilize the cards you create on Privacy.com: visiting their desktop site, installing the browser extension, or using their mobile app. In any case, all you’ll need to do is copy the credit card number (or debit card, actually) it assigns to you — complete with expiration date and security code — as your payment info when checking out of an e-commerce site.

To make this easier, all you’ll need to do is click on the card number and Privacy will automatically copy it to your clipboard. For mobile app users, the same functionality can be accessed by tapping and holding on the card (single tapping will merely toggle the full card number display on and off). As for the expiration and CVV, you’ll need to enter those manually.

I mentioned above that Privacy.com does offer a browser extension. There are two main ways that this tool can help make your checkout process easier. The first is that you can click the Privacy extension icon on the right side of your browser to gain quick access to your Wallet in order to view existing cards or create new ones. You can also click the “Transactions” tab to easily view recent purchases you’ve made with your cards.

However what makes the extension even more helpful is that, when you encounter a checkout form asking for a card number, a little Privacy.com icon may appear in the card number field. Clicking this will then launch a tool allowing you to select or create a new card and have the information automatically entered for you. For that reason alone, if you use Chrome or Firefox and end up signing up for Privacy.com, I’d recommend installing this extension as well.

Making changes to your cards

It should also be noted that you can make a number of changes to your Privacy.com cards at any time. Among the options at your disposal is the ability to pause your card from being used, increase or decrease your spending limit, switch a funding source, or delete a card entirely. All of these can certainly come in handy as you start to actively use the service.

Spend limits

Something I didn’t notice when I initially reviewed Privacy.com is that there are weekly and monthly spending limits. Considering that these are prominently on your dashboard, I’m guessing it’s something that’s been added more recently. In any case, according to the site’s FAQ, these limits are determined on a per-account basis. More specifically, they note that those who frequently use their accounts, have recurring payments set up on the site, and/or who reach their spending limits will see increases to these caps.

To give you an idea of what to expect, it’s been a few months since I’ve used my Privacy.com card and my limits are $100 a week and $400 a month. Those seem pretty low but not ridiculous. Then again, if you were planning on making a purchase over $100, I do wonder if an automatic increase would be possible. Hopefully you won’t need to find out, I guess!

Sharing cards

Another interesting feature on Privacy is the ability to share a created card. To do this, just select a card, tap the three dot icon, choose “Share,” and then enter the person’s email address. This will then email them a link they can click to view the card info — and they don’t even need their own Privacy account in order to access it.

In terms of potential use cases, if you wanted to loan someone money or give them what is essentially a universal gift card, you could simply create a one-time use card, set a spending limit, and send it to them. Sure there are other options for accomplishing similar goals, but I think this is a pretty neat feature nonetheless. Of course, you will want to use discretion in who you send cards to and will want to adhere to Privacy’s terms and policies, which you will need to agree to before proceeding with your card share.

Pro and Teams Plans

While Privacy.com’s main service is free to use for individuals, the site also offers upgraded plans. The first of these is the $10-a-month Pro plan. At this tier, you’ll be able to generate up to 36 cards a month (instead of the regular 12), receive priority support, and more. Plus — perhaps more importantly — you’ll earn 1% cashback on your first $4,500 in purchases using Privacy.com cards.

Meanwhile the Teams plan comes at a cost of $25 a month. In addition to a dedicated account management, this plan allows for up to 60 cards to be created a month. Moreover the site says that features such as Multi-user support and exports to software such as Quickbooks and Xero will be coming to this tier in the future.

Although the Teams option may be attractive to some small businesses, I’m guessing most individuals will just want to stick with the free plan. Then again, if you do manage to spend enough using Privacy, you could end up covering the $10 fee (and then some) with the Pro plan’s 1% back. So, if you’re thinking it over, you can learn more about each plan on Privacy’s Pricing page to help make your decision.

How Privacy.com Could Save You Money

Protecting you from fraud

The most obvious way that Privacy.com could potentially save you money is by helping protect you from fraud. When retailers or other entities get hacked, your credit card information could be exposed. Thus, by using a proxy card number, you’re limiting what funds thieves can get access to if they should attempt to utilize this stolen data.

I’d be remiss if I didn’t mention that similar technologies are already being employed outside of Privacy’s tool. From digital wallets like Apple Pay to EMV chip cards, transactional tokens are quickly becoming the new norm. That said, not all of these same protections extend to e-commerce, which is where Privacy.com comes in.

Keeping track of your memberships and subscriptions

Have you ever signed up for a free trial and forgotten about the service until several months and hundreds of dollars later? This is actually something that Privacy.com could potentially help prevent as well. By using one-time cards to sign-up for free trials, you can ensure that you won’t see subsequent charges that you don’t want. Of course, you should always follow up and formally cancel any trials that unintentionally convert to memberships so you don’t continue to receive annoying emails from companies demanding your money.

A similar benefit is that Privacy.com could help you keep track of all the various subscriptions you do have. I’ve long advocated for making a master list of memberships and periodically reviewing them to see where cuts can be made — now Privacy can essentially recreate that functionality, complete with sleek-looking logo cards to boot. Plus, by setting your monthly spending limits to match what your charges should be, you can bet you’ll be notified if the cost of your subscription were to suddenly go up, allowing you to consider whether the service is still worth the hiked price.

Referrals and cashback

Finally, like many financial tools and apps these days, Privacy.com incentivizes users to spread the word. First, by sharing your custom referral link with friends, family, and whomever else, they’ll receive $5 in credit that can be utilized when they make their first purchase using the platform. Better yet, you’ll also receive a $5 credit when they sign-up and complete their first qualifying transaction. You can get $5 for yourself by signing up through my link here.

The other way that you can be rewarded for sharing Privacy.com is with their Cashback Key. With a Cashback Key code, you’ll be entitled to earn 1% back on all of the purchases you make using Privacy.com cards over the span of one month. Oddly, while you can access the part of the page where you can enter a Cashback Key you’ve received, it doesn’t really explain how to obtain them. Thus, while I’m still not 100% sure on how these Cashback Keys are doled out, they do seem to be tied to promotions — including potentially involving referrals.

The Pros and Cons of Privacy.com

Pro: Greater security when shopping online

In my eyes, the premise of Privacy.com is a strong one. Although most of the major e-commerce sites you visit are secure, breaches are still all too common. While I’m certainly no expert, the tool that Privacy has built seems like a smart solution and one worth trying.

Con: You need to trust the site in order to sign up

On the other hand — and as I mentioned — it’s not hard to imagine that some would-be users might be scared off by needing to enter their banking login info before getting started. After all, that data getting out could lead to more damage than a credit card number being revealed.

Of course Privacy.com realizes this conundrum and addresses it in their FAQ section. Regarding the need to log into your bank account, they write, “It sounds risky. But give us a sec to explain how this works. We partner with Plaid to facilitate these connections. Plaid has an agreement with your institution to be a trusted bridge to your bank. When you login via the portal provided by your bank, we are given a token by your bank that allows us to verify your account and conduct Privacy related transactions. We don’t obtain or store your login information, and you can change it anytime without affecting your use of Privacy.” So, if that information helps ease your worries, great. If not, I completely understand.

Pro: Helps you keep track of subscriptions and memberships

If I’m being completely honest, I actually see the real benefit of Privacy not as a tool for protecting your card numbers but for keeping up with all of your subscriptions. From the popularity of streaming services to the numerous SaaS applications some of us may try once and forget about, there’s plenty of opportunities to introduce “money leaks” into your budget that can start to add up. Sure my master list plan works well enough, but Privacy streamlines the whole operation and installs plenty of fail-safes to ensure these costly recurring fees don’t slip through the cracks.

Con: No credit card rewards

Now that we’ve highlighted what I think is the biggest advantage of Privacy.com, I have to mention what I see as its largest drawback — and the one that will likely hinder how much I actually end up using the service. Currently, the only funding sources you can link to cards you create are bank accounts and debit cards. While this makes sense, it’s a big bummer for people like me who earn significant cashback or rewards from credit cards. As a result, it doesn’t really seem worth it to me to use Privacy cards for these services.

Even if there were a way to link credit cards to Privacy’s proxy cards, it’s unlikely that purchases would be categorized by merchant code, which could still cause issues for those looking to maximize rewards. Because of this, while I’ll still utilize Privacy.com for free trials or the occasional transaction where I want some added protection, I don’t foresee using the platform frequently until a solution to the rewards dilemma emerges.

Con: Some have had negative experiences

While I can really only speak to my own experience for my reviews, I’d be remiss if I didn’t share a gripe from a friend of mine. Although they enjoyed the Privacy experience overall, they were surprised to log in one day and learn that their account had been closed. After getting in touch with customer service, they found an odd reason for their ban: too many referrals. No recourse or further explanation was offered and their account was not reinstated.

This story was really interesting to me because it seems quite silly that the site would be concerned about someone bringing them “too many” new customers. Luckily, I suspect that this is a pretty specific incident that not too many people will encounter. Still, I thought it was worth mentioning just in case.

Alternatives to Privacy.com

Although Privacy.com was honestly the first digital one-use card platform I’d ever heard of, since I wrote my initial review, the popularity of this idea has really exploded. Now, there are several options available. That said, unlike Privacy which allows you to link an external bank account to create virtual cards, many of the other options available are integrated into specific banking platforms.

Among the accounts I’ve used that offer virtual card support are Cred.ai, Revolut, Current, and more. Plus, Capital One operates a service called Eno that allows users to generate one-time use cards on the fly while online shopping. This one is particularly interesting to me as it enables customers to earn the rewards from their Capital One credit cards whereas the other options mentioned are debit cards.

Overall, while these platforms may not quite offer the same thing that Privacy does, they may prove to be good alternatives for the right people.

Final Thoughts on Privacy.com

I’m honestly quite surprised I hadn’t heard of Privacy.com before I initially reviewed them — although that was several years ago now. In that time, I’ve seen the popularity of virtual cards grow tremendously alongside other more secure payment methods, such as mobile wallets (which may also use tokenized card numbers). As a result, these days, I don’t find myself using Privacy.com too much. That’s partially due to a lack of credit card rewards but also just feeling as though I don’t need to use the service as much.

Nevertheless, there’s no doubt that Privacy’s platform can benefit some online shoppers. From an easy-to-use browser extension that makes filling out card forms simpler to the ability to manage your budget more effectively, there are multiple benefits to what Privacy has built that make it worth checking out. So whether you want to keep track of your subscriptions and transactions or make an identity thief’s job just a little bit harder, Privacy.com may be able to help you out.