UPDATE: Curve has now been discontinued in the United States. Below is my initial review.

Credit card rewards are great, but working to maximize those rewards can be daunting at times. Not only might your quest require you to carry around multiple cards wherever you go but you’ll also need to remember to use the “right” card for any given transaction. Given this reality, wouldn’t it be nice if you could just use one card to make all of your purchases and have those transactions sent to the best card with the best rewards? That’s the pitch of Curve — a U.K.-based company that recently launched in the United States.

For the past couple of months, I’ve been trying out the U.S. version of Curve and putting it to the test. What I found is that, for the most part, it lives up to its promise. So, how exactly does Curve work and what else does it have to offer? Let’s take a look at the card, including some pros and cons.

Using Curve: What Makes it Unique

What is Curve?

Curve is a card that allows you to link many of your existing credit and debit cards in order to consolidate and automate your rewards. By creating Rules and other features, you can use Curve to pay for transactions and effectively have those purchases forwarded to your selected card. This way, you can make sure to maximize rewards on every purchase without needing to carry several different cards.

That’s the basic idea of Curve, but let’s dive into the details.

How does it work?

Curve essentially acts as an intermediary when you make transactions. You use your Curve card online or in stores and then Curve charges the card you desire. While this is an online transaction, Curve will carry over the original transaction Merchant Category Code. Because of this, you should be able to earn all of the rewards your credit cards feature, including those offered in specific categories. On top of that, Curve customers earn 1% back in the form of Curve Cash whenever they use the card to make a purchase – for a limited time, that is. Currently, the Curve site notes that this introductory offer is for three months from the time cardholders open an account.

Currently, there are limits to what types of cards can be linked to Curve. These include:

- Visa debit cards

- Mastercard debit cards

- Mastercard credit cards

- Discover debit cards

- Discover credit cards

- Diners Club credit cards

In the United States, Curve is issued by Hatch Bank.

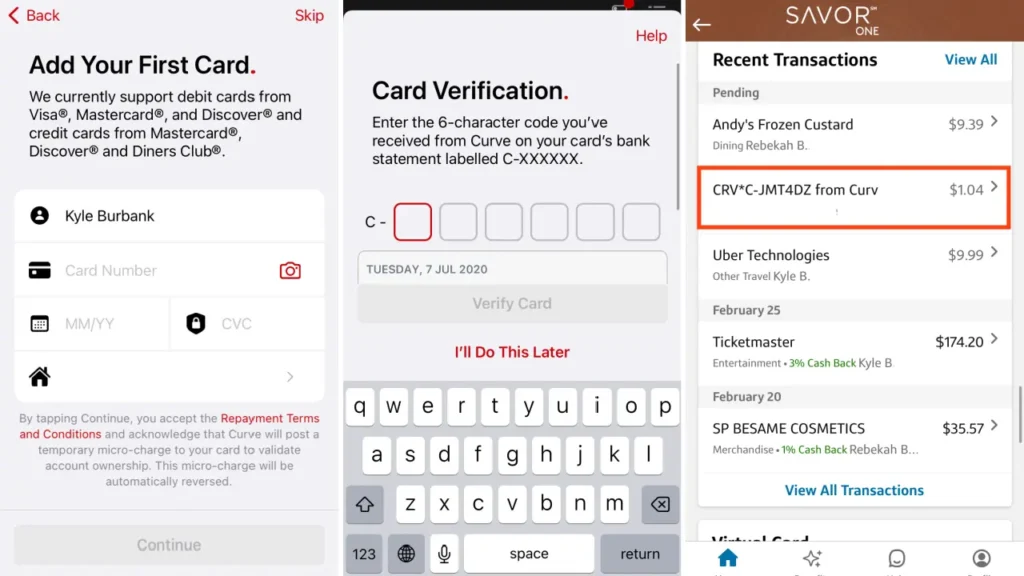

Applying for the card

To get started with your Curve application, you’ll need to download the app, enter your phone number, and confirm said phone number. Then, you’ll need to provide some personal information, such as your name, date of birth, home address, and Social Security number.

Now is a good time to mention that Curve does need to check your credit in order to approve you. However, this is only a “soft pull,” meaning that it won’t show up as an inquiry on your report. Nevertheless, as I learned, you will need to make sure your credit reports aren’t frozen so that Curve can access them. Also, while I didn’t have an inquiry display on my report, the account itself was added to my Equifax report after it was opened.

If approved, you’ll also be required to confirm the terms and cardholder agreement. After that, you’ll be ready to start using Curve.

Physical metal card

To my surprise, the card featured on the site wasn’t quite what I received. Instead, I received a nice, sleek, black metal card — which also came in a fancy box. Not that I need all of my cards to be metal, but this one does look and feel quite nice. One minor quibble, however: the Curve logo on the front is opposite from the mag strip on the back. Thus, I’m never sure what direction the card should be in my wallet. Yes, this is petty, aesthetically particular, and largely inconsequential, but that’s really all I got.

I should note that according to the pop-up I got when applying, these black metal cards are limited. So, if you don’t get one, I apologize in advance.

Adding cards

The process of adding cards to Curve is quite easy but also fairly unique. First, you’ll simply enter your card’s number, including the expiration date and CVC. There’s also a camera tool if you want to attempt to auto-populate this info by scanning your card.

Next comes the fun part. To verify your card, Curve will create a temporary transaction on the card you’re attempting to link. Attached to this transaction will be a code. So, in the Curve app, you’ll be prompted to enter that code as a means of verification. After you do so, the transaction will be reversed, so there’s no need to worry about the funds (unless it’s a debit card and you’re very low on funds… I’m not 100% sure how that would work, but I wouldn’t recommend it).

Creating rules

A major way that Curve helps you maximize your credit card rewards is through Smart Rules. In the app, you tell Curve what card it should use for purchases in popular categories such as Food & Drink, Entertainment, Groceries, Travel, and more. Alternatively, you can also set Smart Rules that are based on the size of a transaction. When combining Rule types, you can also rank them in order of priority.

In the event you want to ignore rules temporarily and select a specific card, you can do that as well. Just go to the Smart Rules tab and toggle off the option. Then, you can swipe through and tap the card you want to use as the new default.

While these basic rules are great, they are quite limited. For example, I wanted to create a rule for Warehouse Clubs as this is one of my Discover It card’s rotating categories for Q2 2023. Alas, Curve doesn’t have a Warehouse Clubs specific category. For the record, I did try changing the category of a previous Sam’s Club transaction to Health and then setting a Discover rule for this category instead but that didn’t work either. The good news is that, once I did put the purchase on the correct card, the proper cashback did apply. Nevertheless, I’d love to see an expansion of rule options in the future just to make things that much easier.

Redeeming Curve cashback

As I mentioned, every time you use Curve during your first three months, you’ll earn 1% back in Curve Cash. These funds can then be redeemed for purchases. In fact, you can toggle on an option to have Curve automatically tap your cashback reserve if you make a transaction that can be fully covered by your balance. If you don’t opt for this, you can simply choose to pay with your Curve Cash card when you’re ready. That said, it doesn’t seem as though you can split tender or redeem for credit otherwise. Lastly, according to Curve’s FAQ, the transaction will need to be for more than 10¢ to use your cashback.

Now is when I need to admit that I wasn’t fully aware that the 1% back was only an introductory offer. Apparently, I hadn’t hit that mark when I first reviewed the service (and still haven’t). I suppose this welcome bonus of sorts is better than nothing, but I’m still disappointed that it’s not really a permanent feature — and that I was dumb enough to miss this distinction before applying.

Crypto rewards

For those who’d rather earn cryptocurrency instead of fiat cashback, Curve has you covered. By going to Card Information for the Curve Cash card, you tap Select Token in order to earn rewards in a number of supported assets, including Bitcoin, Ethereum, Litecoin, and more. Note that these crypto services are powered by Zero Hash.

Personally, I haven’t looked into this feature more than that as I’m not really feeling the whole crypto scene at the moment. Instead, I’m quite happy to just stick with regular cashback. But, if you’re a true believer, then you can HODL your cashback in your coin of choice.

Curve Credit

When you open up a Curve card, you’ll also be opening up a Curve Credit card. From what I can tell, the idea here is that should your transaction be declined for some reason, Curve will instead put it on your Curve Credit. This is what they call Anti-Embarrassment Protection. Of course, if your transaction amount exceeds your Curve Credit limit, you’ll still be declined — and, with my limit only being $500, this does seem like a distinct possibility.

Honestly, of everything that Curve has to offer, this is the feature I feel could easily be dropped. I’ll explain why I feel that way a bit more later but, for now, just know that it exists. And, no, I haven’t actually used it.

Go Back in Time

Finally, another cool feature of Curve is the ability to Go Back in Time. Just like Cher, you can turn back time by swapping a purchase from one card to another. That’s heavy.

Okay, I’m done with time travel references, so let’s talk about what this actually means. Basically, should you decide to use the Time Travel feature, Curve will refund the card you initially used to make a purchase and will instead charge a different one. It’s still very cool — but perhaps not quite as advanced as you might be led to believe.

There are also some limitations to the Time Travel feature. For one, you can only do it once a transaction has posted and not when it’s pending. That’s kind of a letdown because, if you’re anything like me, you remember the moment after you make a purchase that you should have used a different card. Rather than fix it at the moment, you’ll need to remember to wait a day or two and then use Time Travel.

Another restriction is that you can only use the feature up to 30 days after the transaction date. Lastly, you can only use Time Travel once per transaction. Should that last restriction slip your mind, Curve does do a good job of reminding you repeatedly that this will be your one and only shot at changing the past, ensuring that your final answer is a good one.

Despite these rules, I think this is an incredibly useful feature — and one I’ve had to tap a couple of times already.

My Experience with Curve: Pros, Cons, and Potential Uses

Making purchases

It should be obvious, but the process of paying with Curve is extremely simple: you just pull out the card (or the digital version on your mobile wallet) and use it to buy goods or services. Really, the front end of the experience looks identical to any other credit card. That’s because all of the fancy stuff is on the back-end — AKA the app.

On that note, something else I really like about using Curve to pay is how quickly the notifications arrive. For example, I might use the card at a gas station, see the authorization charge, and then immediately get the updated total when I’m done pumping. These alerts also show you what card it ultimately charged, giving you a heads up in case you do need to use Time Traveler after the fact. Speaking of that…

Time travel

One of the big questions I had in regards to the Time Travel feature was what the date on the transaction would be. As it turns out, it’s not that complicated: the posted date will be the date on which the Time Travel feature is used. So, if you make a purchase on April 28th and use the feature on May 3rd, the new transaction date would be May 3rd.

Now, I’m not going to completely spell out why this is important or how such knowledge could be useful. However, for those who are a bit more daring, this could be a fairly powerful feature. I, on the other hand, want to be a bit more cautious and use my cards as close to intended as possible.

Earning rewards

I have great news to report: each of my Curve transactions has resulted in the correct rewards I was expecting. As promised, the original merchant codes carried over to my transactions without issues. In fact, the only desirable difference is that “CRV*” is added before the merchant name with Curve transactions. Given this experience, I’m inclined to say that Curve works as intended. Plus, the introductory bonus 1% back in Curve Cash has been great, making Curve my go-to card for most transactions during my initial few months. I suspect that will remain the case even when this bonus does sunset for me.

Supported cards

As I mentioned in the earlier section, Curve doesn’t work with all existing credit cards — with the biggest exceptions being Visa credit cards or any American Express cards. That latter one is the biggest bummer for me as my Amex Gold is my best choice in categories such as dining or groceries. On the other hand, thanks to the 1% bonus I’ve been getting from Curve, suddenly my Capital One SavorOne matches the 4x I get from the Gold (depending on how you value Membership Rewards points). Also, in all honesty, it’s not that hard to carry a couple of extra cards around with me. So, while I’d welcome the addition of more cards to Curve, it’s far from a dealbreaker for me.

What does the future hold?

Here’s the thing about Curve: it’s almost too good to be true. Naturally, this leads me to worry that things could take a turn in the future — especially given my history with FinTechs. Yet, in this case, I’m actually more concerned about the response from other issuers rather than a pivot from Curve themselves.

It’s not hard for me to imagine that Curve’s abilities could be used to abuse the rewards features of certain credit cards. In turn, if the card were to gain enough popularity, it’s not hard to imagine that issuers might work to disallow not only these more flagrant abuses but also Curve transactions in general. After all, it wouldn’t be hard since every transaction is marked “CRV.”

I’m not going to pretend that I’m educated enough to even know if Curve is technically violating issuer policies by adapting the merchant code on transactions. But, I do feel smart enough to know that card companies will be willing to take action if they are. All this is to say that, while I’m loving Curve currently, I do think there’s at least some amount of risk involved with the product.

Final Thoughts on Curve

In many ways, Curve is a product I’ve been dreaming of for some time. Even better than options such as Coin that allowed customers to easily select what credit card they wanted to use at any given time, Curve also allows you to pre-plan or delay that moment of decision while earning you bonus cashback. It certainly sounds like a dream, but it really does work… for the most part.

While I’ve experienced very few issues with Curve during my time using the tool, there have been a couple. This includes encountering a couple of declined transactions — this despite the fact that Curve is meant to provide “anti-embarrassment protection” via its Curve Credit. Luckily, I was able to simply pay with another card, but I’m curious why the card ran into issues in the first place.

Speaking of Curve Credit, I really wish there were a way to opt out of this feature. Personally, I don’t feel the need to have a back up so it’s just unnecessary. Furthermore, since this does show up as an account on your credit report, getting the Curve card does take up a “5/24” slot. If you don’t know what that means, basically it just refers to an apparent policy from a major issuer that suggests you can’t get any of their cards if you’ve added more than five accounts to your report in the past two years. Having seen how important this is to credit card enthusiasts, I could see it being a major deterrent for some.

Finally, as I mentioned, I do have some concerns about the future. Perhaps those are unfounded, but they do worry me. On that note though, I suppose it’s almost a good thing that Amex isn’t supported by Curve as they’re the issuer I’d most be worried about upsetting.

With all of that said, despite these current and potential downsides, I’ve still been pretty thrilled with Curve overall. Therefore, in spite of my concerns, I really hope that the platform only continues to improve and thrive. As for whether you should apply, if you don’t mind losing a 5/24 spot and are willing to accept the risks I’ve laid out, I think it may be worth a shot.