Back in the late 90s and early 2000s, you may have heard the term “peer to peer” as it related to music sharing services like Napster. About a decade later the term gained new popularity in an entirely different field altogether: finance. More specifically, lending.

Peer to peer (P2P) lending is a model that matches up borrowers in need of loans with investors willing to fund them. This system benefits both parties by offering lower rates for borrowers and significant returns for investors. As a result the sector has grown tremendously in recent years as word continues to spread, companies grow, and technologies improve.

In this comprehensive guide we’ll take a look at some of the most popular peer to peer lending platforms and how they differ from each other, share advice for borrowers considering a P2P loan, and offer tips for investors looking to make a healthy return on their money:

A Look at Six Peer to Peer Platforms for Investors

Today there are several different peer to peer platforms of varying sizes. Furthermore each company has their own way of doing things. This includes their algorithms for approving borrowers, the way their loans are graded, and what types of loan products they offer.

Let’s take a look at six different platforms and what they each have to offer:

Lending Club

Since starting in 2007 Lending Club has grown to become the largest peer to peer lender, having facilitated over $45 billion in loans. In addition to personal loans, the company also offers small business loans, auto refinancing, and patient solutions.

- Offers personal loans for up to $40,000, business loans up to $500,000

- Has seven grades of loans (A-G)

- Average investor returns across all note grades: 5.94%

- Projected charge-off rates for A-graded loans: 2.06%

Prosper

Prosper was founded in 2005, making it one of the first P2P lenders in the space. Since then the company has funded more than $15 billion in loans. In addition to its multiple personal loan options, Prosper has announced it plans to offer home equity lines of credit (HELOCs) starting later this year.

- Offers personal loans between $2,000 and $40,000

- Loan terms of 36 or 60 months

- Grades include AA, A, B, C, D, E, and HR.

- Historical average investor return: 5.3%

Upstart

Founded in 2014, Upstart has since funded $3.7 billion in loans. The company, created by former Google employees, prides itself on using more factors in their decision process, including education, area of study, and job history.

- Offers personal loans from $1,000 up to $50,000

- Average APR on a 3 year loan is 19%

- 87.5% of Upstart loans are either current or paid in full

Funding Circle

Originally started in the United Kingdom, Funding Circle began operating stateside in 2013. Overall the company has originated more than $9.5 billion in loans globally. At this time, Funding Circle focuses exclusively on business loans.

- Offers small business loans for up to $500,000

- Loan terms range from 6 months to 60 months

- Historical average return rate for investors is 5.3%

- Minimum investment is $25,000

Peerform

According to their “About Us” page, Peerform was founded in 2010. Like other peer to peers, they cite the lack of lending from major institutions as their inspiration for finding a solution. The platform was actually purchased by Versara Lending in 2016 and now operates as an affiliate company of Versara.

- Only open to institutional investors purchasing entire loans

- Peerform loans have 16 grades, ranging from DDD to AAA

- APRs for loans range from 5.99% to 29.99%

- Offers a customization tool for investors to adjust their loan portfolio to their risk tolerance

StreetShares

StreetShares is a bit different than the other platforms on this list. Instead of offering investors the chance to purchase a piece of a specific small business loan, they sell Veteran Business Bonds. These bonds then fund loans that will benefit small businesses that are at least 25% owned by a veteran or military spouse or has a veteran or military spouse as the co-guarantor.

- Bonds can be purchased with as little as $25

- Veteran Business Bonds have an interest rate of 5%

- There is a 1% fee for withdrawing before one year

- StreetShares has originated more than $100 million in loans and $470 million in contract financing

Real Estate Crowdfunding Platforms for Investors

While the initial wave of peer to peer platforms mostly focused on personal and small business loans, more recently, attention has turned to real estate. Today several platforms allow individuals to invest in real estate via crowdfunding. Let’s take a look at four such platforms and how they work.

Fundrise

Officially launched in 2012, Fundrise says it intended to lower the costs, improve the quality, and broaden the access of real estate investing. The company has positioned real estate investing as part of “modern portfolio” that goes beyond the typical mix of stocks and bonds. Since its debut, the platform’s users have invested a total $2.5 billion in real estate.

- Open to accredited and non-accredited investors over the age of 18 who are U.S. citizens

- Historical annual returns of 8.7% to 12.4%

- “Starter Portfolio” allows investors to begin with as little as $500

- Core plans include Supplemental Income, Balanced Investing, and Long-Term Growth

Realty Mogul

With an emphasis on earning passive income, Realty Mogul positions itself as an alternative to traditional real estate investment. While they note that investors should always do their own due diligence, they explain that the company “conducts rigorous due diligence and provides asset management on all its properties offering a truly passive investing experience.” The platform offers both “MogulREITs” (Real estate investment trusts) as well as private placement deals.

- MogulREITs require minimum investments of $5,000

- Private Placement minimums vary and are only available to accredited investors

- Distributions can be automatically reinvested or deposited to a bank account

- MogulREIT I has an annualized basis return of 8% while MogulREIT II has an annualized basis return of 4.5%

Patch of Land

Billed as a Peer-to-Real-Estate — or “P2RE” — lending marketplace, Patch of Land matches investors and borrowers much the same way traditional P2Ps do. In fact, the platform lists specific properties that investors can contribute funds to. As a result, the site says borrowers can receive funding in as little as seven days.

- Only available for accredited investors

- Average APR for investors is 10.56%

- Loan originations total $725 million through Q3 2018

- Average loan size is $457,000

PeerStreet

Peerstreet is a platform that allows individuals to invest in real estate backed loans. These loans are assessed by a team of finance, real estate experts, and of course algorithms to provide what they deem to be the highest quality investments to its users. Earlier this year, PeerStreet announced that the platform has transacted $2 billion and currently managed more than $1 billion in assets.

- Only open to accredited investors

- Users can invest as little as $100

- Investors can select loans individually or automatically using investment criteria

- Historical annualized returns of 6% to 9%

For Borrowers — What to Consider When Seeking a P2P Loan

Partially by coincidence and partially by design, many peer to peer lending platforms emerged in the aftermath of the 2008 banking crisis, which led to several intuitions scaling back their lending operations. While loan approval rates at the big banks have since rebounded some, the need for alternatives is still strong. That’s why more and more individuals and small businesses are turning to peer to peer and other online lenders seeking funds.

If you’re considering obtaining a personal or small business loan from a P2P platform, here’s what you should be aware of:

What to use P2P loan funds for

The vast majority of personal loans obtained on peer to peer platforms go towards one thing: debt consolidation. Because credit card interest rates are infamously high, often times paying off card balances with a loan can help save consumers some cash. In fact Lending Club has previously reported that their borrowers save an average of 35% in interest compared to their credit cards while Upstart pegs customer savings at 23%.

Of course paying off existing debt isn’t the only use for P2P loans. Other popular reasons for borrowing include big-ticket purchases, home renovations, and other expenses. Plus, even if loans aren’t specifically billed as “business loans,” personal loans can also be used as capital.

Research the platform before applying

While there are several reputable lending platforms — like the ones mentioned above — that operate exclusively online, there are unfortunately some scammers out there as well. To combat this threat it’s easy to conduct a quick search and see what information you can find on the company. You’ll want to look for media coverage from reputable sites (Reuters, CNNMoney, TechCrunch, VentureBeat, etc.), which regularly cover FinTech companies. This will help you determine if a company is legitimate before you share sensitive information with them. Additionally you should never give a lender money upfront for a loan.

Preparing to Apply

Before applying for your loan there are a few things you should take care of. The first step is to obtain a copy of your credit report. Be sure to review your report for any errors that might be hurting your scores and rectifying them with the bureau reporting prior to applying for your loan. Additionally sites like Credit Karma will give you a ballpark idea of what your credit scores look like, which will help you to determine the likelihood of your application being approved.

Speaking of credit, while most P2P platforms allow you to retrieve your loan rate quote via what’s called a “soft pull” or “soft inquiry” that won’t impact your credit score, you’ll want to confirm this is the case before sending your request. “Hard pulls” or “hard inquiries” will display on your credit report and could have a negative impact on your score — especially if you have several in a short period of time. Therefore it’s always a good idea to double check.

Another important step to take before applying is to calculate how much you can afford to pay per month. Most P2P lenders will require you to pay back your loan with monthly installments, thus it’s paramount that these payments fit into your budget. Failing to make these payments will not only hurt your credit scores but could also end up costing you more money in the long run. That’s why you should never take out a loan you can’t afford or don’t have a clear repayment plan for.

Calculate your costs

One advantage that peer to peer lenders have is a limited amount of overhead thanks to the absence of physical branches. Thus they are often able to offer loans to well-qualified borrowers at lower interest rates. That said, if you’re credit isn’t in the best of shape, you may end up paying a premium on your loan.

When you look at loan options, make note that there’s a difference between interest rates and APR (annual percentage rates). The APR not only includes the loan’s interest rate but also accounts for other fees and charges. As a result, this figure will give you a better idea of how much it will actually cost you to borrow.

Another thing to watch out for are origination fees. These are typically assessed to you at the time you take out the loan and amount to a percentage of your total loan. For example, if you were approved for a $10,000 with a 5% origination fee, you would actually only receive $9,500. However you would still be responsible for paying back the full $10,000 plus any interest, fees, etc. Keep this in mind when figuring out how much money to apply for as well as for determining the best deal.

Shopping around

Speaking of finding the best deal, there’s no harm in trying multiple platforms to see if they can offer you a better rate than another one could. In most cases, on again, applications should be a “soft pull” until you actually accept the loan. As mentioned, be sure to compare interest rates, APRs, and origination fees as well as other factors like the length of the loan, how much you can borrow, pre-payment penalties, etc. when making your final decision about which lender to go with.

The peer to peer process

Once you accept a loan from a peer to peer lender, keep in mind that the process may not be over. That’s because your loan still needs to be funded by investors. This can take hours, days, or, in some relatively rare cases, your loan may not be filled at all. Luckily, as P2P and the FinTech sector as a whole continues to grow, the likelihood of your approved loan going unfunded are falling and the most requests are filled quickly.

For Investors — Tips for Earning the Best Returns on P2P

If you’ve ever read a book doling out financial advice there’s no doubt that you understand the importance of investing. Furthermore a quick look at the current landscape will inform you that your investment options are now more plentiful than ever. Peer to peer lending is among those emerging choices and continues to attract new investors.

Since peer to peer lending is still a fairly new concept to many, there’s a good chance you’re wondering what some of the best practices are and how to achieve the best results. With that in mind, let’s take a look at a few tips to get you started investing in P2P and potentially earn 10% or more on your investment:

Diversify

You’ve almost assuredly heard it said that the key to investing is having a diversified portfolio. The same could be said about investing in peer to peer loans. This not only means avoiding putting all of your eggs in the P2P basket (you should consider a mix of investments in stocks, bonds, mutual funds, real estate, etc.) but it also applies to spreading your money out across many different loans within your peer to peer lending investment.

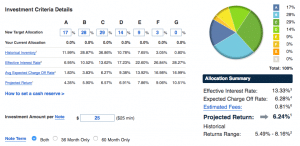

While default rates for P2P loans are relatively low (and vary by credit rating) there is always the risk that your borrower will fail to make their payments. Because of this it’s much better to contribute $100 towards 100 loans than it is to pony up $10,000 to one borrower. That’s why most peer to peer platforms allow you to put small amounts of money towards any given loan. For example the minimum contribution per loan on both Lending Club and Prosper is a mere $25.

The biggest reason for diversifying your peer to peer loan investments is so that you can control your risk and even customize it to your level of tolerance. This can be achieved by looking at how a given platform grades their loans and then selecting whom you choose to lend to. Obviously lending to borrowers with lesser credit will earn you a larger interest rate but will also bring a higher risk for default. As a result it’s wise to offset these gambles by also buying loans from more creditworthy borrowers.

Diversification isn’t just smart in theory — there are also stats that show how such strategies pay off for peer to peer investors. According to Lending Club, 99% of their investors who invest in more than 100 loans (with no one loan making up more than 1% of their account) see positive returns. Like any investment, this still presents risk but P2P can be a comparatively safe investment when done right.

But can people really earn 10% or more on their investments? The answer is yes. A number of people have achieved those results. You can read one first-hand example here.

Do your research

Many of the top peer to peer lenders, including Lending Club, Prosper, and Upstart, offer some form of automated investing. While these options can be great down the road, being hands on at the beginning and learning to navigate the platform for yourself can help you give you a much better idea of where your money is going.

“Getting your hands dirty” by starting your investment manually will serve you well long term. Any type of automated loan buying you do will require you to set investment parameters. But how will you know what settings are important if you don’t know what you’re looking for.

That’s why it makes sense for new investors to experiment and see what works for them in terms of both macro goals – maximizing return vs. minimizing risk, as well as individual loan efficiency, e.g. state of origination, purpose of loan, term of loan, etc. Each individual value may or may not have an effect on your big picture goals. Tracking performance by exact criteria manually at the beginning can help you setup your automated investment parameters for long term investing.

Keep your money working for you

With any luck you’ll start to see your account growing as the loans you’ve invested in are paid back. It’s an exciting feeling for sure but don’t forget to put that money back to work! Reinvesting your gains will allow you keep interest payments flowing into your account instead of having your money just sitting there.

As mentioned many platforms will offer automated services that can make it easy to ensure that your funds are always being reinvested. But, if you’re taking the manual route, just be sure to keep an eye on your balance and buy new loans as you can.

Also consider using your “found money” to experiment with buying different types of loans than you normally purchase. Who knows — maybe you’ll stumble upon a new favorite factor. Even if you use automated tools it’s always a good idea to make some manual loans to test new parameters. You may find trends that aren’t yet built into the automated models – arbitrage plays that will increase your overall return.

Consider a self-directed IRA

One of the biggest reasons people choose to invest is so that they have money available when they’re ready to retire. Typically accounts such as 401(k)s, IRAs, and others are invested in stocks, bonds, and mutual funds, but did you know that you can also put your IRA money towards buying peer to peer loans? With a self-directed IRA you can choose exactly what you’d like to invest your money in including P2P platforms.

Self-directed IRAs have the same tax benefits as traditional IRAs, making them a great option for funding your peer to peer investment account. Additionally self-directed Roth IRAs, where you pay taxes upfront instead of upon withdrawal, are also available. Best of all, in the interest of diversification, you might also be able to leave a portion of your retirement balance in your current IRA while rolling over some funds to a new self-directed account that you can use to buy loans.

Conclusion

Even though it’s existed for nearly a decade now, peer to peer lending isn’t quite mainstream just yet. Still the industry continues to grow rapidly as more and more borrowers and investors learn about the advantages P2P holds for both parties. While getting started might seem overwhelming at first, by utilizing these tips and doing your own research you’ll be ready to submit your borrowing application or open your investment account in no time. Good luck.