The “buy now, pay later” scene has a new entrant. This week, Zilch announced its arrival in the United States. According to the company, the app launched with 150,000 pre-registered customers and comes after the service gained two million U.K customers since its debut there 18 months ago. Elsewhere, Zilch has raised $400 million in debt and equity from Goldman Sachs among others and the company is valued at more than $2 billion.

Like other “buy now, pay later” platforms, Zilch allows users to pay off purchases in four payments made over six weeks. While customers will need to pay 25% of their balance at the time of purchase, subsequent 25% payments are due two weeks, four weeks, and six weeks after the transaction. Alternatively, however, Zilch customers can elect to use the platform to pay for their purchase in full upfront and earn 2% in Zilch Rewards as a result.

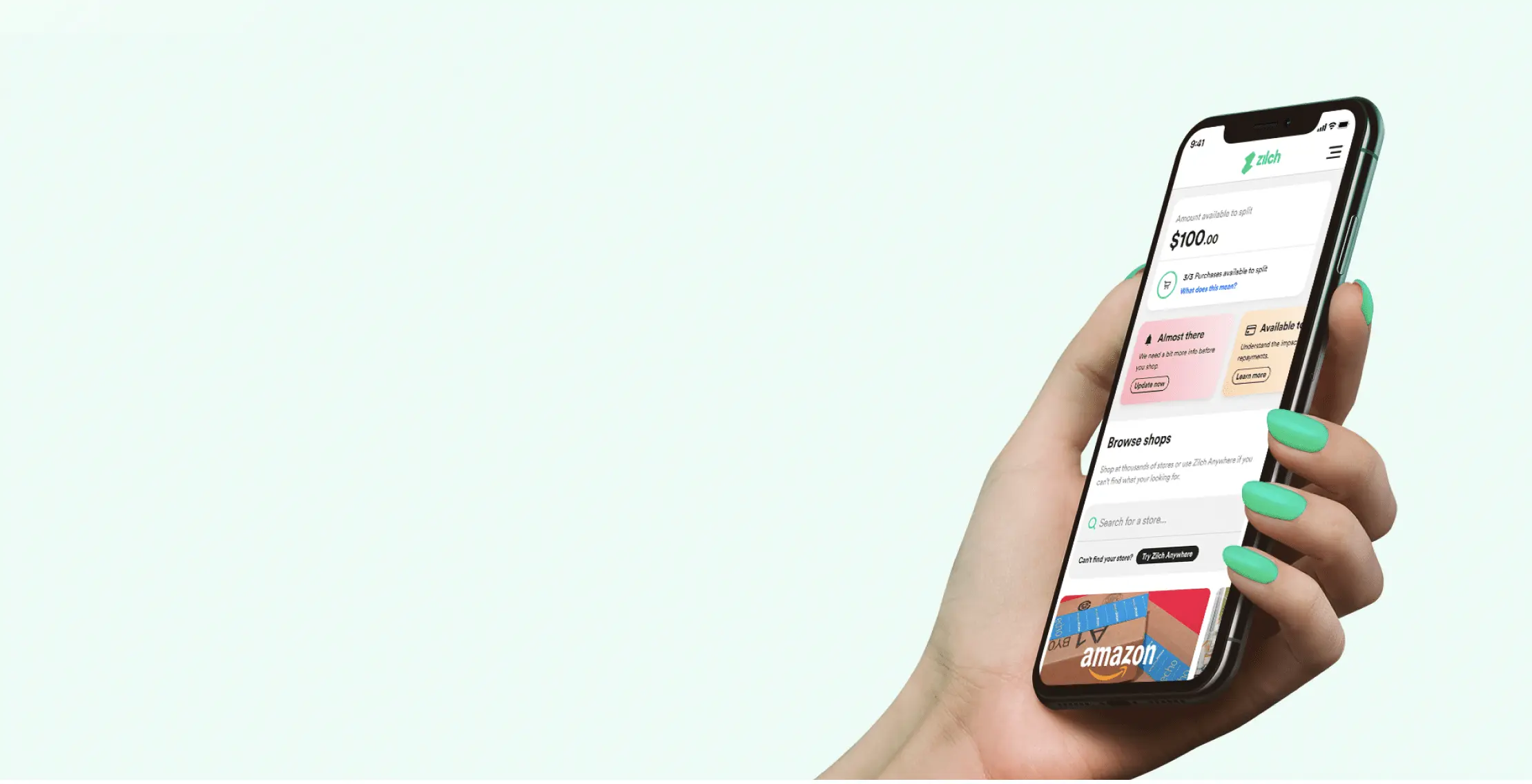

To get started with either option, customers can select the store they plan on shopping in (or select the Zilch Anywhere option), choose their payment plan, and generate a Zilch card, which is accepted anywhere Mastercard is. From there, users are able to manage payments and turn on Auto Billing in the app. Notably, loans through Zilch USA are made by Cross River Bank — a FinTech-friendly bank that recently raised a $620 Series D.

Speaking to the idea behind Zilch, the company’s co-founder and CEO Philip Belamant said in a statement, “In 2020, U.S. consumers paid $120 billion in fees and late charges to credit cards, which we believe is unacceptable and fundamentally misaligned with the interests of consumers. They are being set up to fail and need more flexibility, especially during a cost of living crisis and a time of surging inflation, to pay for goods and services how and when they want – with a system that avoids late payments and unnecessary, onerous fees.”

Belamant went on to note the company’s success and what led them to America, saying, “Our experience in the U.K., and the survey we conducted here in the U.S., make it clear that U.S. consumers want much more from BNPL providers, what we call BNPL 2.0 – which removes what consumers dislike (lack of ubiquity/fees and/or late charges). Zilch also gives what consumers say they value – cashback, which can be used to discount larger purchases.”

Ultimately, while Zilch might position itself as “BNPL 2.0,” there’s not much that differentiates it from the field — at least not on the surface. While the 2% cashback option is interesting, it’s currently not exactly clear what Zilch Rewards can be redeemed for, which would definitely impact the appeal. Furthermore, with the “buy now, pay later” field growing ever more crowded, it will be interesting to see if Zilch can continue the momentum it’s seen in the United Kingdom. Of course, on that note, only time will tell.